Last month we ran a free audit on a contractor's books.

We pulled his Profit and Loss statements going back three full years and walked through them line by line.

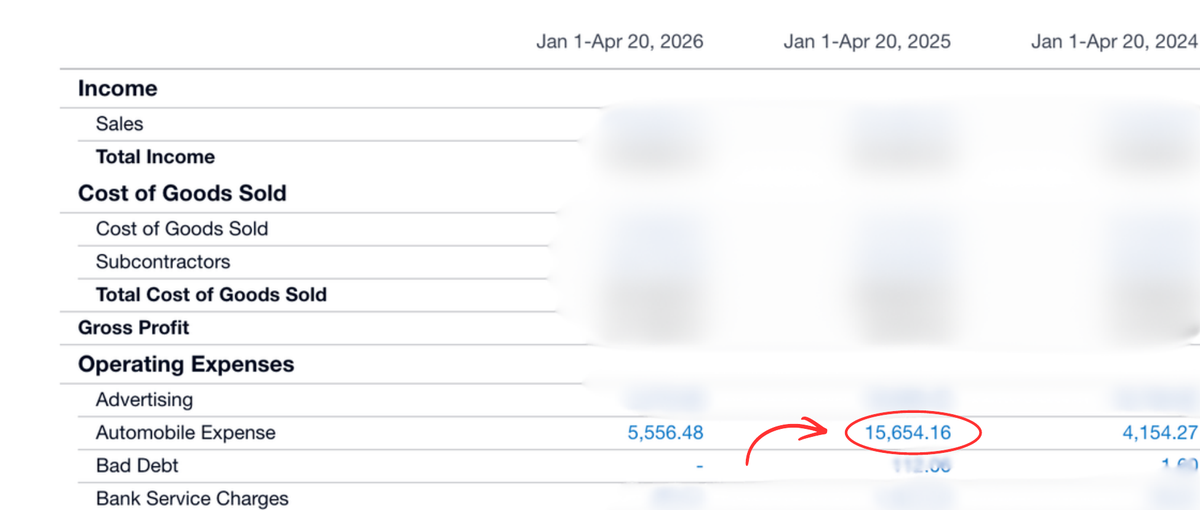

One number didn't follow the pattern.

Automobile Expense, 2025: $15,654. The year before, $4,154. A 4× jump in one year, no business reason for it.

So we clicked in.

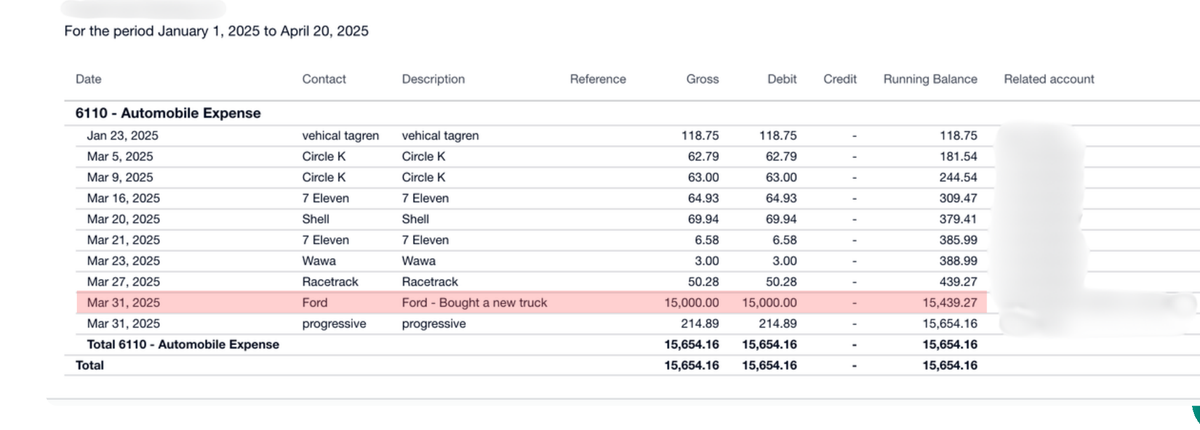

One line. March 31, 2025. Ford. Description: bought a new truck.

A truck. For $15,000. Sitting in Automobile Expense.

But this wasn't even the real problem.

We kept scrolling.

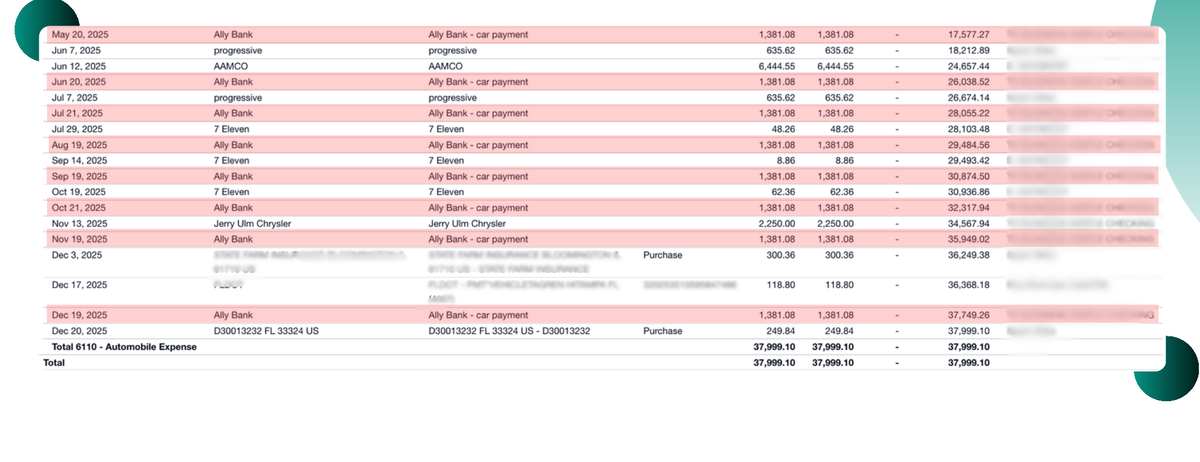

Every month after the purchase, an Ally Bank line for $1,381. Car payment. Going straight into Automobile Expense too.

He financed the truck. And every monthly payment was being booked as an expense.

One truck purchase. Four errors in his books.

-

The truck wasn't booked as an asset.

It went to Automobile Expense instead of the balance sheet.

-

The loan wasn't booked as a liability.

Nothing on the balance sheet showing what's owed to Ally Bank.

-

The loan payments weren't split.

Only the interest is an expense. The principal pays down the loan — it's not a deduction. Instead, the full payment was hitting expenses every single month. He was effectively expensing the truck twice.

-

No depreciation schedule.

The truck should be written off over five years. There was nothing.

Here's what this costs him.

Tax side

When the IRS catches the double-expensing — back taxes. Penalties. Interest.

Deduction side

Five years of clean depreciation write-offs — lost.

Lender side

No truck on the books, no loan on the books. When he goes for a line of credit or to bond the next big job, the bank is making real decisions off numbers that aren't real.

This is what happens when a generalist touches construction books.

If you've ever financed a truck, a trailer, equipment — anything — some version of this could be sitting in your books right now.

How we cleaned up a contractor's messy books & set up job costing

A real client. Before-and-after numbers. The exact steps we took.

Book your free 48-hour audit

A construction-CPA team walks through your books, flags what's miscoded, and shows you the fix.

Get next week's article free.

Every Friday. Job costing, WIP, cash flow — and the bookkeeping mistakes generic accountants miss. Unsubscribe anytime.

Subscribe to FinTruction Insights